Luke Darkow is a Portfolio Manager at Aperture Investors, bringing over 13 years of experience in investing with a specialization in litigation finance private credit investments. Throughout his career, he has been instrumental in sourcing, analyzing, structuring, and managing investments, deploying more than $1 billion into the litigation finance asset class. Luke leverages a well-established network of plaintiff law firms and legal service providers to access and originate opportunities within this specialized field.

Before Aperture, Luke was a Principal and Portfolio Manager at Victory Park Capital, where he led a litigation finance asset-based lending strategy. His background also includes roles at TPG Capital and Morgan Stanley, further enriching his expertise in finance and investment management. Luke holds a B.S. in Business Administration with a focus on Finance – Applied Investment Management from Marquette University.

Company Name and Description: Aperture Investors is an alternative asset manager founded by Peter Kraus, focusing on specialized credit and equity strategies across global markets. The firm aims to generate compelling returns in capacity-limited strategies, emphasizing a client-centric approach. Aperture operates as part of the Generali Investments ecosystem, combining boutique agility with large-scale resources. Aperture supports private credit litigation finance, structured credit, and diverse equity strategies, managing over $3 billion in assets.

Year Founded: Founded in 2018 by Peter Kraus in partnership with Generali Group, one of the largest global insurance and asset management companies

Headquarters: Headquartered in New York with offices in London and Paris

Area of Focus: Aperture Investors approaches litigation finance through a private credit perspective, prioritizing capital protection and steady income by utilizing structured term notes. These notes are backed by diversified, settled, or short-duration legal claims, offering lower volatility than traditional litigation funding, which depends on individual case outcomes and carries higher uncertainty and risk.

We primarily focus on lending against legal claims that are either post-settlement or procedurally mature, near-settlement, and/or short-duration. This approach emphasizes secured lending on more predictable claims to reduce volatility and enhance income stability

Member Quote:"The litigation finance asset class generally exhibits minimal correlation with broader capital markets, is highly inefficient, and continues to grow as demand for legal funding exceeds available capital, creating a compelling opportunity for private credit lenders like Aperture Investors."

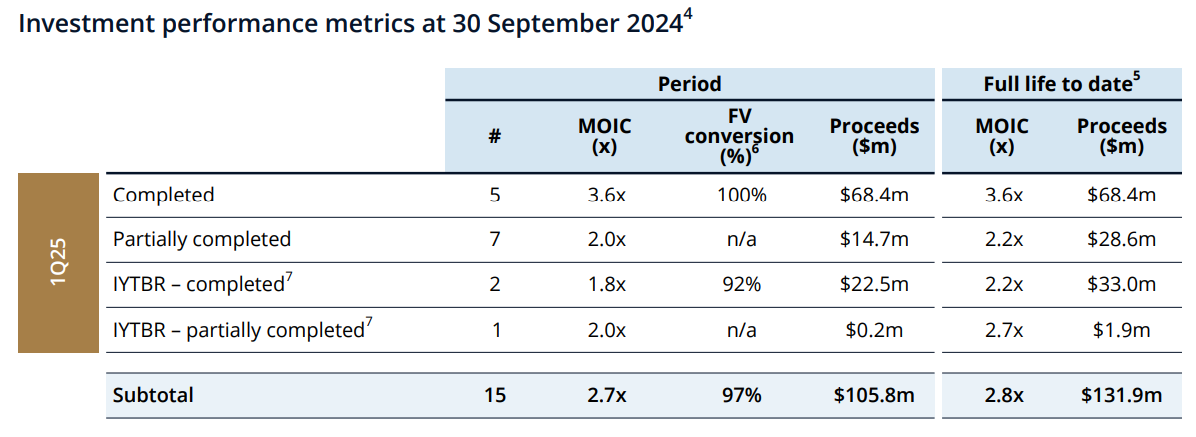

Omni Bridgeway Limited (ASX: OBL) (Omni Bridgeway, OBL, Group) announces the key investment performance metrics for the three months ended 30 September 2024 (1Q25, Quarter).

Summary

Investment proceeds of A$105.8 million in 1Q25; A$14.2 million provisionally attributable to OBL1, excluding management and performance fees.

Performance fees of A$9.7 million received during the Quarter2.

Management, transaction and equivalent fees of A$5.9 million during the Quarter.

15 full and partial completions in the Quarter, delivered an overall multiple on invested capital (MOIC) of 2.7x.

7 full completions during the quarter had a combined fair value conversion ratio of 97%3.

A$129 million in new fair value added from A$138 million of new commitments.

Strong pipeline, with agreed term sheets outstanding for an estimated A$198 million in new commitments, if converted.

Transaction fees have successfully been included in nearly all new commitments made in FY25 and/or negotiated in new term sheets.

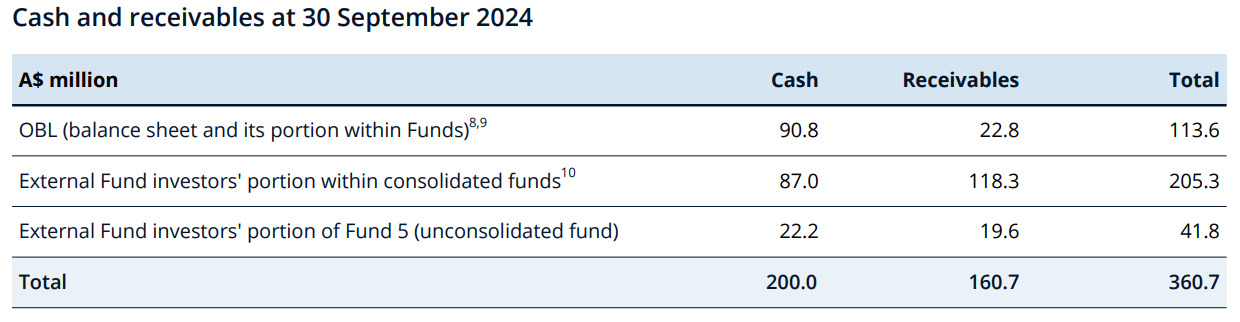

OBL cash and receivables of A$114 million at 30 September 2024.

A$0.8 billion of fair value in potential completions over the next 12 months.

Good progress in relation to the strategic focus areas of cost optimisation and secondary market transactions.

Key metrics and developments for the Quarter

Income and completions

During the Quarter, five full completions and seven partial completions were recognised, and two full completions and one partial completion were recorded as income yet to be recognised (IYTBR), resulting in proceeds of A$105.8 million for the quarter, with A$14.2 million provisionally attributable to OBL (excluding management and performance fees1).

The overall MOIC on these 15 full and partial completions during the quarter (incl. IYTBR) was 2.7x.

The seven full completions during the Quarter (incl. as IYTBR) had a combined fair value conversion ratio of 97%.3 The fair value conversion ratio for all 31 fully completed investments (excl. as IYTBR) since transitioning to fair value per 31 December 2023 is 111%.

New Commitments

As per the date of this report, new commitments of A$138 million were made to 10 new investments as well as to a number of investments with increased investment opportunities. This level, proportionate to the full year target, reflects the typical northern hemisphere seasonality, and is in line with prior years.

Total new commitments include A$28 million of potential external co-fundings for new investments originated and managed by OBL. OBL will be entitled to separately agreed management fees, transaction and performance fees on such external co-funding.

The fair value associated with these new commitments is A$129 million.

Strong pipeline of 34 agreed exclusive term sheets, representing approximately A$198 million in investment opportunities.

Transaction fees have been successfully included in the majority of new commitments made and term sheets signed in FY25. Transaction fees have typically been structured as a combination of an upfront fee and an annual recurring fee at or exceeding on average 2.5% of the investment commitment (in total over the life of the investment).

Portfolio review

As at 30 September 2024, A$0.8 billion of fair value is assessed to potentially complete in the 12 months until 30 September 2025 (12 Month Fair Value). The 12 Month Fair Value is the proportionate part of our total book fair value, which has expected cash inflows over the applicable 12 month period based on the underlying probability weighted net cash flows fair value models. All, part or none of these investment inflows may eventuate during the 12-month period.

Corporate

As announced during the full year results presentation on 29 August 2024, the current strategic focus is on cost optimisation, and fair value validation through completions and secondary market transactions.

Secondary market discussions on multiple assets are progressing well. A status update will be provided at the semi-annual results presentation or through specific prior ASX announcements.

At 30 September 2024, the Group held A$113.6 million in cash and receivables (A$71.2 million in OBL balance sheet cash, A$1.0 million in OBL balance sheet receivables and A$41.4 million of OBL share of cash and receivables within Funds).

In aggregate, at 30 September 2024 OBL had approximately A$114 million to meet operational needs, interest payments, and fund investments before receiving any proceeds from investment completions, secondary market sales, management and transaction fees, and associated fund performance fees.

Footnotes

Represents indicative cashflows (excluding management and performance fees) from the Funds to OBL in connection with the investment completions. It represents the aggregate estimate of the cash distributed and yet to be distributed under the various distribution waterfalls of the Funds assuming investment proceeds are gross cash proceeds. The Fund's capital status and waterfalls operate on a cash collection and distribution basis and do not align with the accounting treatment. Accordingly, the income and NCI attribution disclosed in the Group Consolidated Financial Statements will not necessarily match this.

Performance fees received are subject to clawback arrangements, to ensure that performance fees ultimately reflect actual fund returns and applicable hurdles. As a result, accrual of performance fees for accounting purposes will generally occur in a later period to the cash receipt.

The fair value conversion ratio indicates the ratio of cash proceeds and deployments in connection with completed investments, discounted back to the date of the last reported portfolio fair value (30 June 2024 currently), compared to the reported fair value of such completed investments as at that prior reporting date.

All metrics presented are on a full investment basis, excluding the impact of co-investments or partial secondary sales. This reflects a change in methodology from market disclosures prior to FY25, and better reflects the performance of the investments originated, underwritten and managed by the Group.

Full life to date metrics include any partial completions in prior periods for the investments involved.

Relates to full completions recognised and yet to be recognised during the Quarter.

IYTBR reflects the status as per 30 September 2024. If a matter was originally reported as IYTBR for a period and has been recognised as revenue in a later quarter, it is no longer reported in this table as IYTBR in the initial period.

Includes Funds 2&3, Fund 4, Fund 6, and Fund 8 and represents OBL's portion of each respective Fund.

Includes Fund 5, which is not consolidated within the Group Consolidated Financial Statements, and represents OBL's 20% interest.

Includes Funds 2&3, Fund 4, Fund 6, and Fund 8 and represents the external investors' portion of each respective Fund.

Further information

Further information on terms used in this announcement is available in our Glossary and Notes:

The Glossary and Notes contain important information, including definitions of key concepts, and should be read in conjunction with this announcement.

The investments of Funds 2&3, Fund 4 and Fund 6 are consolidated within the Group Consolidated Financial Statements, along with the interest of the respective external fund investors.

The investments of Fund 8 are consolidated within the Group Consolidated Financial Statements. Fund 1 was deconsolidated on 31 May 2023; its metrics, effective from this date, are not disclosed in this document. The Fund 4 IP portfolio was deconsolidated on 8 December 2023 following the sale of a 25% interest in these investments.

Fund 1 and Fund 5 are not consolidated within the Group Consolidated Financial Statements; the residual interest in Fund 1 and in the Fund 4 IP portfolio are recognised as an investment in associate, Fund 5 is brought in at the Group’s attributable 20% share of income, assets, and liabilities. Throughout this document, Fund 5 is presented at 100% values (except where otherwise stated) for consistency of presentation across OBL's funds.

Commitments include conditional, and investment committee approved investments. This report includes a number of concepts, such as fair value and income yet to be recognised, which are classified as a non-IFRS financial measure under ASIC Regulatory Guide 230 “Disclosing non-IFRS financial information”. Management believes that these measures are useful for investors to understand the operations and financial condition of the group. Unless expressly stated, this non-IFRS financial information has not been subject to audit or review by BDO in accordance with IFRS.

The figures presented in this document are based on preliminary data and have not been audited. While every effort has been made to ensure the accuracy of the information, these figures are subject to change and should not be considered final.

This announcement is authorised for release to the market by the Disclosure Committee.

NorthWall Capital ("NorthWall"), a leading credit investment firm delivering private capital solutions to counterparties in Western Europe, today announces the appointment of Shannon Cody as Head of Business Development, EMEA. Shannon will focus on strengthening relationships with existing global institutional investors, while expanding the firm's client base through new partnerships. Her efforts will play a key role in driving capital growth across NorthWaII's core strategies, which include Opportunistic Credit, Senior Lending, Asset-Backed Lending and Legal Assets.

Shannon brings with her over 15 years of experience in business development roles at leading financial institutions. Most recently as Head of EMEA Business Development at Mudrick Capital Management, she led the firm's business development, sales and client services across EMEA and APAC. Shannon was pivotal in growing Mudrick's London office, spearheading campaigns focused on distressed and stressed credit strategies. Prior to this, Shannon held senior roles at Barclays and Morgan Stanley, where she led capital introduction efforts across Europe.

Fabian Chrobog, Founder and Chief Investment Officer at NorthWaII Capital, said: "We are thrilled to welcome Shannon Cody to NorthWall at this exciting time for our firm. Her extensive experience in establishing long-term partnerships with investors will be crucial as we continue to expand our footprint across EMEA. Shannon will help us deepen relationships with our institutional investor base as we continue to scale our flagship credit strategies."

Shannon Cody, Head of Business Development, EMEA at NorthWaII Capital, said: "I am excited to join NorthWall and look forward to working with the team to expand our presence across the region and drive continued fundraising success."

Earlier this year NorthWaII announced the final close of its flagship North Wall European Opportunities Fund Il and associated vehicles attracting more than €640m in investor commitments, surpassing its initial €500m target and more than doubling the size of its predecessor vintage.

In an announcement from the Civil Justice Council (CJC), the Litigation Funding Working Group has published the Interim Report and Consultation for its review of litigation funding. As laid out in the report’s foreword, the publication of the Interim Report represents the first phase of the working group’s efforts, and therefore does not contain any recommendations at this stage. The purpose of the Interim Report is to provide the background to the issues being examined, as well as providing the context for the questions in the Consultation.

The report itself is divided into six parts, which are as follows:

The Development of Third Party Litigation Funding in England and Wales

The Development of Self-Regulation of Third Party Litigation Funding

Different Approaches to Regulation

Approaches to Regulation in Other Jurisdictions

The Relationship between Costs and Funding

Funding Options

Each of these parts is further divided into two sections, with the first section acting as a brief overview of the topic that covers the ‘Key Points’. The second section provides an in-depth exploration of these issues, including examples of relevant case law and drawing upon existing research and studies covering third-party litigation funding.

The Consultation, which represents the second phase for the working group includes a list of 39 questions which consultees are encouraged to answer, divided into the following categories:

Questions concerning ‘whether and how, and if required, by whom, third party funding should be regulated’ and the relationship between third party funding and litigation costs.

Questions concerning ‘whether and, if so to what extent a funder’s return on any third party funding agreement should be subject to a cap.’

Questions concerning how third party funding ‘should best be deployed relative to other sources of funding, including but not limited to: legal expenses insurance; and crowd funding.’

Questions concerning the role that should be played by ‘rules of court, and the court itself . . . in controlling the conduct of litigation supported by third party funding or similar funding arrangements.’

Questions concerning provision to protect claimants.

Questions concerning the encouragement of litigation.

General Issues

The consultation period is now open and will run for three months, closing on Friday 31 January 2025 at 23:59.

The publication of the Interim Report and Consultation is accompanied by the following statement from Sir Geoffrey Vos, Master of the Rolls, Head of Civil Justice and Chair of the CJC:

“I welcome the publication of the CJC’s interim report and consultation on litigation funding. Litigation funding plays an important role in ensuring access to justice. I am grateful to co-chairs Dr John Sorabji and Mr Justice Simon Picken, and their working group for this report. I encourage all interested parties to read the report and respond to the consultation, which will run until Friday 31 January 2025. I look forward to the publication of the Working Group’s final report in summer 2025.

“It is a busy and exciting time for the CJC, which is also conducting a review of the Solicitors Act 1974, through a working group chaired by Mr Justice Adam Johnson. The CJC understands that there will be areas of overlap between the work of that group and the Litigation Funding Group. It will create valuable consistency and coherence for the Solicitors Act Working Group to be able to take account of the responses to this Consultation by the Litigation Funding Group as they take forward their work in the new year.”

Following the conclusion of the consultation period, the third and final phase will begin, during which the Working Group will prepare and then submit its Final Report and Recommendations to the CJC. The Interim Report confirms that the current timeline still expects for the Final Report to be delivered and published by the summer of 2025.

The Interim Report’s appendices also include a full list of the members for both the Working Party and the wider Consultation Group, listed below.

Working Party

Mr Justice Simon Picken (CJC member) – Co-Chair, Dr John Sorabji (CJC member) – Co-Chair, Mrs Justice Sara Cockerill, Professor Christopher Hodges OBE (Regulatory Horizons Council), Lucy Castledine (Financial Conduct Authority), and Nicholas Bacon KC.

Wider Consultation Group

Alistair Kinley (Director of Policy & Government Affairs, Clyde & Co), Professor Andrew Higgins (CJC member; Professor of Civil Justice Systems, University of Oxford), Dr Mark Friston (Barrister, Hailsham Chambers; Bar Council Representative), Jackie Griffiths (Head of Regulatory Policy, Solicitors Regulation Authority), Jamie Molloy (Head of ATE, Ignite Speciality Risk), Jennifer Morrissey (Partner, Harcus Parker; Law Society Representative), Julian Chamberlayne (Partner, Stewarts) Kenny Henderson, (Legal Adviser, Fair Civil Justice; Partner, CMS Cameron McKenna Nabarro), Lucy Anderson (Senior Lawyer, The Consumers’ Association (Which?)), Neil Purslow (Chair of the Executive Committee, International Legal Finance Association; UK CIO, Therium Litigation Funding), Professor Neil Rickman (Professor of Economics, University of Surrey), Nicola Critchley (CJC member; Partner, DWF), Professor Rachael Mulheron KC (Hon) (Professor of Tort Law and Civil Justice, Queen Mary University of London), Rhea Gupta (Legal and Policy Research Consultant, Class Representatives Network), Stephen Wisking (Partner, Herbert Smith Freehills), Suganya Suriyakumaran (Legal Services Board), Susan Dunn (Director, Association of Litigation Funders; Head of Litigation Funding, Harbour Litigation Funding), Tajinder Bhamra (Interim Head of Civil Litigation Funding and Costs Policy, Ministry of Justice), and Tom Steindler (Managing Director, Exton Advisors).

Following the publication and adoption of the Voss Report by the European Parliament, industry participants and observers have been waiting to see how the European Union would potentially proceed towards a new legislative framework for regulating third-party funding.

An insights article from Deminor, authored by Patrick Rode and Joeri Kline, looks at the mapping study conducted by the European Commission on the state of third-party litigation funding across the EU. The article first provides an overview of the Commission’s study, in terms of the issues the study explored and its aims, before going on to offer some additional insights into Deminor’s contributions to the study and the funder’s view on the future of European funding regulations.

As Rode and Kline explain, the Commission’s study has a broad scope, exploring everything from the volume and types of cases that are being funded, to the nuances of funding arrangements and the returns on investments for funders. They also note that the study is taking into consideration the existing regulations covering funding within each EU member state, analysing the effectiveness of these rules and the parallel impact of funding. On this last point, it is clear the study wishes to explore both the perceived positive benefits of funding, such as widening access to justice, as well as the alleged negative impact of litigation costs.

Rode and Kline share that Deminor “has actively contributed to this debate by submitting its responses to the Commission”, providing information on its own funding engagements whilst also emphasising that its clients “are capable of negotiating and securing transparent and equitable funding agreements.” They go on to say that the funding agreements agreed between Deminor and its clients “ensure fair and market-aligned compensation for Deminor while addressing potential conflicts of interest in a manner that protects the interests of all parties involved.”

Deminor’s article concludes by stressing “the importance of maintaining a balanced approach to regulation – one that preserves the flexibility needed for sophisticated institutional investors while ensuring fairness and transparency for all parties engaged in litigation funding agreements.”

As the debate over disclosure and transparency requirements for litigation funding continue in different jurisdictions across the globe, one US advocacy organization has started a new campaign to act as a focal point for those in favour of introducing a federal disclosure rule.

An announcement from Lawyers for Civil Justice (LCJ) revealed that it has launched a new campaign focused on third-party litigation funding (TPLF) disclosure, called ‘Ask About TPLF’. The initiative calls on courts and parties involved in civil litigation to ask about the presence of any third-party funding in their cases, arguing that it is essential for everyone involved to be aware of potential conflicts of interest and to establish who is controlling the decision-making process in these lawsuits.

LCJ stated that the Ask About TPLF campaign has three objectives:

Advocate for a clear, uniform rule requiring disclosure of TPLF.

Encourage courts and parties to ask about TPLF in their civil cases.

Build the case for a uniform rule by spotlighting the inconsistent – and in some cases inappropriate – responses by courts to motions seeking TPLF disclosure.

According to LCJ, the launch of the Ask About TPLF initiative follows the news that earlier this month, the U.S. Judicial Conference's Advisory Committee on Civil Rules agreed to begin a study into litigation finance, to ascertain whether a federal rule governing disclosure of third-party funding was necessary. LCJ also referenced the letter signed by over 100 companies that called for such a disclosure rule to be introduced in the Federal Rules of Civil Procedure (FRCP).

More information on Ask About TPLF can be found on the campaign’s website, as well as on X/Twitter and LinkedIn.

On the afternoon of September 25, the "International Conference on the Third-Party Funding Industry" was successfully held in Beijingi. The Conference was hosted by the Beijing International Dispute Resolution Center (BIDRC), organized by Houzhu Capital, and co-organized by Dingsong Legal Capital.

The conference received support from the Beijing Arbitration Commission/Beijing International Arbitration Center (BAC/BIAC), China International Economic and Trade Arbitration Commission (CIETAC), China Maritime Arbitration Commission (CMAC), Hong Kong International Arbitration Centre (HKIAC), Singapore International Arbitration Centre (SIAC), and the International Chamber of Commerce (ICC). Other supporting organizations included the Chinese Society of International Law, China-Asia Economic Development Association, China-Africa Business Council, Queen Mary University of London, Burford, Omni Bridgeway, Hilco IP Merchant Banking, Nivalion, Dun & Bradstreet, Caijing, and Law Plus. The Conference attracted over 300 guests in person and more than 60,000 participants online.

Huang Jin, Chairman of the Beijing International Dispute Resolution Center and President of the Chinese Society of International Law, and Yu Jianlong, Vice President of the China Council for the Promotion of International Trade (CCPIT) and Vice President of the China Chamber of International Commerce (CCOIC), delivered opening remarks. The Conference was moderated by Jiang Lili, Commissioner and Secretary-General of BAC/BIAC.

Huang Jin first warmly welcomed and sincerely thanked all participants and supporters on behalf of BIDRC. He stated that this Conference is the first international conference hosted by BIDRC, marking a significant milestone. As the operational entity of the Beijing International Commercial Arbitration Center, BIDRC plays a crucial role in supporting the establishment of the international commercial arbitration center and leading the high-quality development of arbitration in China. He emphasized the need to understand the key trends in the development of international commercial arbitration, including humanization, modernization, internationalization, localization, integration, and digitization. He also stressed the importance of improving a robust arbitration system, cultivating world-class international arbitration institutions, and creating a top-tier business environment characterized by market orientation, rule of law, and international standards. These efforts will enhance China’s foreign-related legal system and strengthen its capacity.

Yu Jianlong highlighted in his speech that, given the profound changes in the international situation and trade patterns in recent years, enhancing corporate competitiveness and strengthening corporate compliance are crucial for promoting high-level opening-up and facilitating the high-quality international expansion of Chinese enterprises. Third-party funding is an important tool for improving companies' ability to address overseas disputes. With the accelerated pace of Chinese companies expanding abroad and the deepening integration of the domestic legal service market with international standards, third-party funding is gradually being accepted and utilized by more Chinese enterprises and legal professionals. He expressed that this conference provides an excellent platform for the industry to explore third-party funding. He hopes participants will strengthen collaboration between academia and practice, deepen their understanding of corporate needs, and continuously learn from international best practices. He also looks forward to fostering cooperation between third-party funding institutions and enterprises.

As a leading scholar in the field of third-party funding, Professor Mulheron from Queen Mary University of London was invited to deliver a keynote speech on the state of third-party funding in England and Wales. Full speech (recording and transcript) available at Houzhu Capital’s WeChat Official Account

In her address, Professor Mulheron examined the rise and evolution of third-party funding in the region, and talked about issues surrounding self-regulation and government oversight within the industry. She provided clear explanations of typical business models in third-party funding, the fee structures for funders, potential costs borne by funders, after-the-event (ATE) insurance, and protections for funded parties. She also offered in-depth insights into cutting-edge issues and perspectives within the field. Professor Mulheron concluded with five key takeaways about third-party funding in England: First, the market is very established and sophisticated, with many funders, brokers and ATE insurers in the market now; Second, third party funding features in both English litigation and arbitration; Third, because of the criteria which funders apply to cases under their business models, only less than 10% of all cases pitched to the funders are funded; Fourth, third-party funding must comply with industry codes of conduct, which include minimum capital requirements for funders; Finally, while England possesses considerable experience in judicial practices concerning third-party funding, there have been debates and disagreements regarding the structure of funding and the validity of funding agreements, and the legislature is taking steps to address relevant issues to further support third-party funding, as it is indeed becoming a huge global market.

During Panel I, Professor Fu Yulin from Peking University Law School served as the moderator. The panelists included Zhang Haoliang, Head of the Business Development Division (International Cases Division) of the BAC/BIAC; Wei Ziping, Director of the Oversight and Coordination Office of CIETAC; Chen Bo, Deputy Secretary-General of CMAC; Yu Zijin, Consultant of HKIAC; Zhang Cunyuan, Director of the China Region of SIAC and Chief Representative of the Shanghai Representative Office; and Huang Zhijin, Director for North Asia and Shanghai Representative Office of ICC. The discussion centered on third-party funding and arbitration rules, drawing on the practices and experiences of the respective institutions. The panelists exchanged insights on recent updates to arbitration rules concerning third-party funding, disclosure requirements, measures to prevent conflicts of interest, and relevant cases processed by their organizations. The panelists concurred that third-party funding is evolving rapidly in practice, and arbitration institutions generally adopt a relatively open stance towards its use in arbitration. They also recognize the necessity for ongoing practice to fully understand the impact of third-party funding on arbitration procedures and rules, with the aim of maintaining the independence and justice of arbitration while better serving the parties.

During Panel II, the discussion was moderated by Fei Ning, Senior Consultant of Houzhu Capital. The panelists included Quentin Pak, Director at Burford; Fu Tong, Co-founder and CEO of Houzhu Capital; Michael D. Friedman, CEO of Hilco IP Merchant Banking; Lau chee chong, Senior legal counsel of Omni Bridgeway in Singapore; Falco Kreis, Senior Investment Manager and Head of the Munich Office at Nivalion; Zhang Zhi, Founder of Dingsong Legal Capital; and Zhu Zhen, Product Sales & Solutions Director of Dun Bradstreet. The panelists discussed third-party funding practices both domestically and internationally, sharing their institutions' experiences across various jurisdictions. They explored a range of topics, including case selection processes and criteria, monetization and funding in the field of intellectual property, the interaction between arbitration rules and funding practices, and risk management for enterprises expanding into foreign markets. They noted that the client base and demand for litigation funding are becoming increasingly diversified, prompting third-party funding institutions to expand their product and service offerings. The panelists expressed optimism regarding the development of third-party funding in China while highlighting unique challenges that the Chinese market faces compared to the international landscape.

During Panel III, the discussion was moderated by Wang Jialu, Co-founder of Houzhu Capital. The panel featured Zachary Sharpe, Head of the Global Disputes Team at Jones Day’s Singapore office; Liu Xiao, Partner of Quinn Emanuel Urquhart & Sullivan, LLP; Zhong Li, Partner of Hui Zhong Law Firm; Wang Zheng, Partner of Hongqiao Zhenghan Law Firm; Li Zhiyong, General Counsel and Chief Compliance Officer of CSCEC International; and Li Lu, Chief Compliance Officer of Essence Securities Asset Management Co., Ltd. The panelists discussed the application of third-party funding, sharing common challenges and solutions they encountered in their past practices, each informed by their specific business contexts. They addressed various issues, including how to set and manage reasonable expectations regarding case progress and outcomes, effectively handle confidentiality and privilege concerns, and navigate disclosures along with related conflicts of interest. In conclusion, the panelists agreed that third-party funding plays a unique role in promoting dispute resolution and accessing justice, especially in bridging the gap between law firms and enterprises in complex cross-border litigation and arbitration.

The successful convening of this conference has established a valuable channel for ongoing communication between domestic and international practitioners and scholars in the field of third-party funding. It has enhanced understanding and awareness of third-party funding within the domestic market and facilitated positive interactions and cooperation among third-party funding institutions, dispute resolution agencies, and relevant users. This will significantly advance the further development of third-party funding in China and make an indispensable contribution to helping Chinese enterprises effectively address cross-border disputes and achieve high-quality development.

The following article was contributed by Tom Webster, Chief Commercial Officer at Sentry Funding.

A Court of Appeal ruling last week is a very positive development for the many consumers currently seeking justice after discovering they were charged commissions that they were not properly told about when they took out motor finance.

With a large number of such claims being brought in the County Courts, the Court of Appeal heard three cases jointly in order to deal with some key issues that commonly arise.

In Johnson v Firstrand Bank Ltd [2024] EWCA Civ 1282, Wrenchv Firstrand Bank Ltd and Hopcraft v Close Brothers, the Court of Appeal foundin favour of all three claimants, allowing their appeals.

The cases concerned the common scenario in which a dealer asks the consumer if they want finance; and if so, the dealer gathers their financial details and takes this information to a lender or panel of lenders.

The dealer then presents the finance offer to the consumer on the basis that they have selected an offer that is competitive and suitable. If the consumer accepts it, the dealer sells the car to the lender, and the lender enters into a credit agreement with the consumer.

The consumer will be aware of the price for the car, the sum of any downpayment, the rate of interest on the loan element of the arrangement, and how much they will have to pay the lender in instalments over the period of the credit agreement. They would expect the dealer to make a profit on the sale of the car. But - at least until the Financial Conduct Authority introduced new rules with effect from 28 January 2021 - the consumer might be surprised to discover that the dealer who arranged the finance on their behalf also received a commission from the lender for introducing the business to them; which was financed by the interest charged under the credit agreement.

In this situation, the dealer is essentially fulfilling two different commercial roles – a seller of cars, and also a credit broker - in what the consumer is likely to see as a single transaction. The commission is paid in a side arrangement between lender and dealer, to which the consumer is not party. Sometimes there might be some reference to that arrangement in the body of the credit agreement, in the lender’s standard terms and conditions, or in one of the other documents presented to the consumer. But even if there is, and even if the consumer were to read the small print, it would not necessarily reveal the full details - including the amount of the commission and how it is calculated.

Turning specifically to the three cases before the Court of Appeal, in one of these, Hopcraft, there was no dispute that the commission was kept secret from the claimant. In the other two, Wrench and Johnson, the claimant did not know and was not told that a commission was to be paid. However, the lender’s standard terms and conditions referred to the fact that ‘a commission may be payable by us [ie. the lender] to the broker who introduced the transaction to us.’

In Johnson alone, the dealer / broker supplied the claimant with a document called ‘Suitability Document Proposed for Mr Marcus Johnson’, which he signed. This said, near the beginning, ‘…we may receive a commission from the product provider’.

Each of the claimants brought proceedings in the County Court against the defendant lenders seeking, among other things, the return of the commission paid to the credit brokers. All three claims failed in the County Courts, but in March this year, Birss LJ accepted their transfer up to the Court of Appeal, directing that the three appeals should be heard together – and acknowledging that a large number of such claims were coming through the County Court, and an authoritative ruling on the issues was needed.

After considering the issues in detail, the Court of Appeal allowed all three appeals. It found the dealers were also acting as credit brokers and owed a ‘disinterested duty’ to the claimants, as well as a fiduciary one. The court found a conflict of interest, and no informed consumer consent to the receipt of the commission, in all three cases. But it held that that in itself was not enough to make the lender a primary wrongdoer. For this, the commission must be secret. If there is partial disclosure that suffices to negate secrecy, the lender can only be held liable in equity as an accessory to the broker’s breach of fiduciary duty.

The appeal court found there was no disclosure in Hopcraft, and insufficient disclosure in Wrench to negate secrecy. The payment of the commission in those cases was secret, and so the lenders were liable as primary wrongdoers. In Johnson, the appeal court heldthat the lenders were liable as accessories for procuring the brokers’ breach of fiduciary duty by making the commission payment.

This ruling will prove hugely significant to the large number of similar claims currently being brought in the lower courts; and Sentry Funding is supporting many cases in which consumers were not aware of the commissions they were being charged when they bought a car on finance.

We can now expect many more such claims to start progressing through the County Courts.

Heather Collins is Chief Investment Officer at Court House Capital and a member of the Investment Committee and is responsible for assessing and overseeing investment opportunities across Australia and New Zealand, as well as identifying and managing a portfolio of funded claims through to resolution.

Heather brings over twenty years’ expertise in legal funding, commercial legal practice and in-house corporate counsel roles. In litigation funding, Heather has underwritten significant disputes. She is a veteran commercial litigator with significant experience advising clients on insolvency, banking and finance, property, construction, Corporations law, trade practices and employment matters. Her client base has spanned industry sectors including property, construction, infrastructure, finance and retail and she has acted for leading consumer brands such as Tiffany & Co, Ralph Lauren, Valentino, Aldi and Sephora.

Heather holds a Bachelor of Arts and Bachelor of Laws (Honours) from the University of Adelaide and is a graduate of the Australian Institute of Company Directors course (GAICD). Heather is the former President of the Women’s Insolvency Network Association NSW branch (WINA) and a Professional Member of the Australian Restructuring & Insolvency Association (ARITA) and the Turnaround Management Association Australia (TMA). She is recognised in Chambers and Partners Litigation Support (2024) and Lawdragon Global 100 Leaders in Litigation Finance (2021-2024).

Company Name and Description: Court House Capital is a leading litigation funder focused on cases in Australia and New Zealand. Court House Capital was established with a mission to provide financial and strategic support to parties seeking capital, risk management and access to justice. Our team is led by industry founders, with Australian based capital, and is renowned for expertise, agility and collaboration.

Member Quote:We offer cost and risk mitigation strategies for commercial clients and ‘a level playing field’ for those who cannot afford to pursue justice themselves. It is an honour to be co-founders of an industry that provides access to justice for so many, and to be the funder of choice for claimants and professional advisers. Our financial resources, industry network and knowledge has helped many claimants achieve successful outcomes.

Sign Up for LFJ’s Weekly Newsletter & Daily Alerts

Thank you for signing up for the LFJ Newsletter!

Stay informed on the latest news and events taking place in the global legal funding space.

You'll now receive the latest global legal funding news, insights, and analysis straight to your inbox.

Please check your email to confirm your subscription.

By completing this form, you agree to allow LFJ to communicate with you per the terms of our Privacy Policy. Your personal information will never be shared or sold to 3rd parties.

Access Premium Content

LFJ members, please log in below to access premium content.