Omni Bridgeway Releases Investment Portfolio Report at 30 September 2024

Omni Bridgeway Limited (ASX: OBL) (Omni Bridgeway, OBL, Group) announces the key investment performance metrics for the three months ended 30 September 2024 (1Q25, Quarter).

Summary

- Investment proceeds of A$105.8 million in 1Q25; A$14.2 million provisionally attributable to OBL1, excluding management and performance fees.

- Performance fees of A$9.7 million received during the Quarter2.

- Management, transaction and equivalent fees of A$5.9 million during the Quarter.

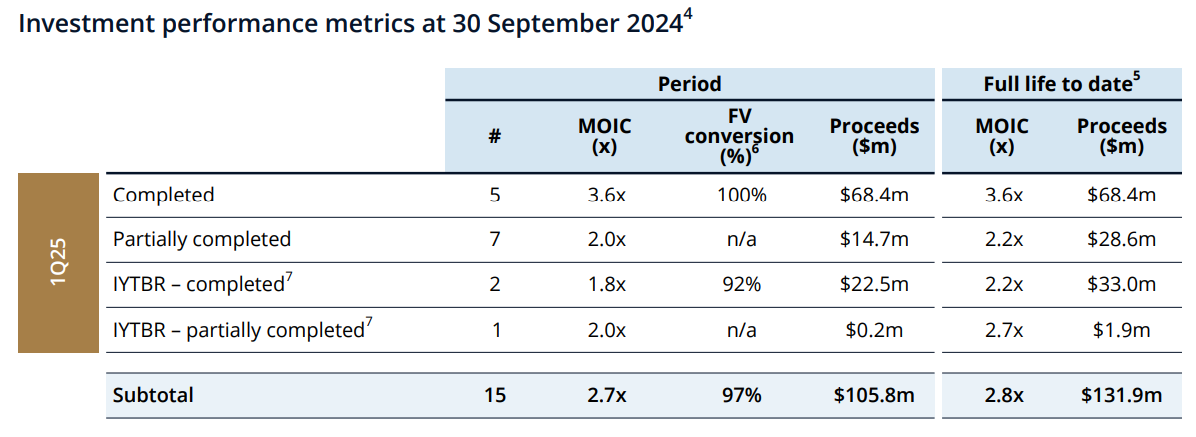

- 15 full and partial completions in the Quarter, delivered an overall multiple on invested capital (MOIC) of 2.7x.

- 7 full completions during the quarter had a combined fair value conversion ratio of 97%3.

- A$129 million in new fair value added from A$138 million of new commitments.

- Strong pipeline, with agreed term sheets outstanding for an estimated A$198 million in new commitments, if converted.

- Transaction fees have successfully been included in nearly all new commitments made in FY25 and/or negotiated in new term sheets.

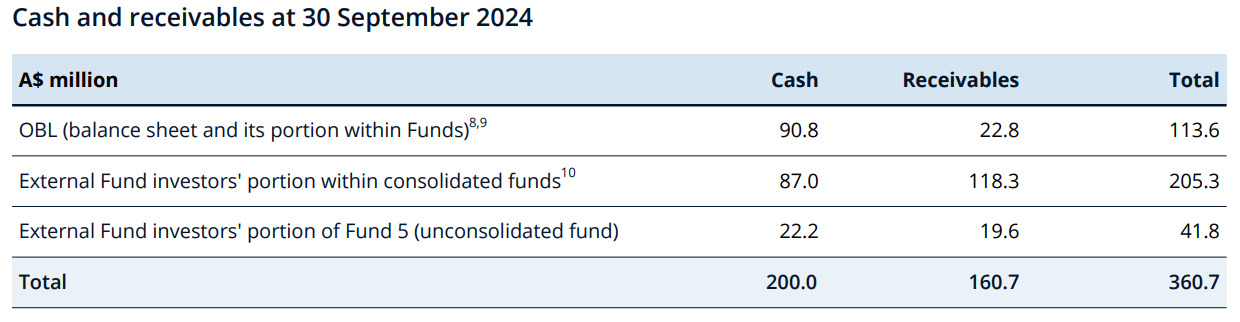

- OBL cash and receivables of A$114 million at 30 September 2024.

- A$0.8 billion of fair value in potential completions over the next 12 months.

- Good progress in relation to the strategic focus areas of cost optimisation and secondary market transactions.

Key metrics and developments for the Quarter

Income and completions

- During the Quarter, five full completions and seven partial completions were recognised, and two full completions and one partial completion were recorded as income yet to be recognised (IYTBR), resulting in proceeds of A$105.8 million for the quarter, with A$14.2 million provisionally attributable to OBL (excluding management and performance fees1).

- The overall MOIC on these 15 full and partial completions during the quarter (incl. IYTBR) was 2.7x.

- The seven full completions during the Quarter (incl. as IYTBR) had a combined fair value conversion ratio of 97%.3 The fair value conversion ratio for all 31 fully completed investments (excl. as IYTBR) since transitioning to fair value per 31 December 2023 is 111%.

New Commitments

- As per the date of this report, new commitments of A$138 million were made to 10 new investments as well as to a number of investments with increased investment opportunities. This level, proportionate to the full year target, reflects the typical northern hemisphere seasonality, and is in line with prior years.

- Total new commitments include A$28 million of potential external co-fundings for new investments originated and managed by OBL. OBL will be entitled to separately agreed management fees, transaction and performance fees on such external co-funding.

- The fair value associated with these new commitments is A$129 million.

- Strong pipeline of 34 agreed exclusive term sheets, representing approximately A$198 million in investment opportunities.

- Transaction fees have been successfully included in the majority of new commitments made and term sheets signed in FY25. Transaction fees have typically been structured as a combination of an upfront fee and an annual recurring fee at or exceeding on average 2.5% of the investment commitment (in total over the life of the investment).

Portfolio review

- As at 30 September 2024, A$0.8 billion of fair value is assessed to potentially complete in the 12 months until 30 September 2025 (12 Month Fair Value). The 12 Month Fair Value is the proportionate part of our total book fair value, which has expected cash inflows over the applicable 12 month period based on the underlying probability weighted net cash flows fair value models. All, part or none of these investment inflows may eventuate during the 12-month period.

Corporate

As announced during the full year results presentation on 29 August 2024, the current strategic focus is on cost optimisation, and fair value validation through completions and secondary market transactions.

Secondary market discussions on multiple assets are progressing well. A status update will be provided at the semi-annual results presentation or through specific prior ASX announcements.

The AGM of the Company will be held in Sydney, on 19 November 2024, and will be in person only. For more information, visit https://omnibridgeway.com/investors/annual-generalmeeting.

Cash reporting and financial position

At 30 September 2024, the Group held A$113.6 million in cash and receivables (A$71.2 million in OBL balance sheet cash, A$1.0 million in OBL balance sheet receivables and A$41.4 million of OBL share of cash and receivables within Funds).

In aggregate, at 30 September 2024 OBL had approximately A$114 million to meet operational needs, interest payments, and fund investments before receiving any proceeds from investment completions, secondary market sales, management and transaction fees, and associated fund performance fees.

Footnotes

- Represents indicative cashflows (excluding management and performance fees) from the Funds to OBL in connection with the investment completions. It represents the aggregate estimate of the cash distributed and yet to be distributed under the various distribution waterfalls of the Funds assuming investment proceeds are gross cash proceeds. The Fund’s capital status and waterfalls operate on a cash collection and distribution basis and do not align with the accounting treatment. Accordingly, the income and NCI attribution disclosed in the Group Consolidated Financial Statements will not necessarily match this.

- Performance fees received are subject to clawback arrangements, to ensure that performance fees ultimately reflect actual fund returns and applicable hurdles. As a result, accrual of performance fees for accounting purposes will generally occur in a later period to the cash receipt.

- The fair value conversion ratio indicates the ratio of cash proceeds and deployments in connection with completed investments, discounted back to the date of the last reported portfolio fair value (30 June 2024 currently), compared to the reported fair value of such completed investments as at that prior reporting date.

- All metrics presented are on a full investment basis, excluding the impact of co-investments or partial secondary sales. This reflects a change in methodology from market disclosures prior to FY25, and better reflects the performance of the investments originated, underwritten and managed by the Group.

- Full life to date metrics include any partial completions in prior periods for the investments involved.

- Relates to full completions recognised and yet to be recognised during the Quarter.

- IYTBR reflects the status as per 30 September 2024. If a matter was originally reported as IYTBR for a period and has been recognised as revenue in a later quarter, it is no longer reported in this table as IYTBR in the initial period.

- Includes Funds 2&3, Fund 4, Fund 6, and Fund 8 and represents OBL’s portion of each respective Fund.

- Includes Fund 5, which is not consolidated within the Group Consolidated Financial Statements, and represents OBL’s 20% interest.

- Includes Funds 2&3, Fund 4, Fund 6, and Fund 8 and represents the external investors’ portion of each respective Fund.

Further information

Further information on terms used in this announcement is available in our Glossary and Notes:

https://omnibridgeway.com/investors/omni-bridgeway-glossary (Glossary)

https://omnibridgeway.com/docs/default-source/investors/general/omni-bridgeway-notes-toquarterly (Notes)

The Glossary and Notes contain important information, including definitions of key concepts, and should be read in conjunction with this announcement.

The investments of Funds 2&3, Fund 4 and Fund 6 are consolidated within the Group Consolidated Financial Statements, along with the interest of the respective external fund investors.

The investments of Fund 8 are consolidated within the Group Consolidated Financial Statements. Fund 1 was deconsolidated on 31 May 2023; its metrics, effective from this date, are not disclosed in this document. The Fund 4 IP portfolio was deconsolidated on 8 December 2023 following the sale of a 25% interest in these investments.

Fund 1 and Fund 5 are not consolidated within the Group Consolidated Financial Statements; the residual interest in Fund 1 and in the Fund 4 IP portfolio are recognised as an investment in associate, Fund 5 is brought in at the Group’s attributable 20% share of income, assets, and liabilities. Throughout this document, Fund 5 is presented at 100% values (except where otherwise stated) for consistency of presentation across OBL’s funds.

Commitments include conditional, and investment committee approved investments. This report includes a number of concepts, such as fair value and income yet to be recognised, which are classified as a non-IFRS financial measure under ASIC Regulatory Guide 230 “Disclosing non-IFRS financial information”. Management believes that these measures are useful for investors to understand the operations and financial condition of the group. Unless expressly stated, this non-IFRS financial information has not been subject to audit or review by BDO in accordance with IFRS.

The figures presented in this document are based on preliminary data and have not been audited. While every effort has been made to ensure the accuracy of the information, these figures are subject to change and should not be considered final.

This announcement is authorised for release to the market by the Disclosure Committee.